ETF Profile

ETF Risk Metrics — Formula Documentation

This document explains the mathematical logic behind the risk fields in the ETF profile API response.

1. Volatility

Definition:

Volatility measures the dispersion of returns for a given asset. It is expressed as the annualized standard deviation of returns.

Calculation Steps:

| Step | Formula | |

|---|---|---|

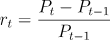

| Returns |  | |

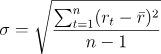

| Standard deviation |  | |

| Annualization |  |

2. SRRI (Synthetic Risk and Reward Indicator)

Definition:

SRRI is based on the annualised volatility of returns and assigns a risk score from 1 (lowest) to 7 (highest) according to predefined bands.

Calculation Steps:

| Step | Formula (Markdown) |

|---|---|

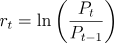

| Log returns |  |

Calculate the standard deviation of log returns and annualise as shown in the Volatility section.

SRRI Bands:

| Volatility Range (σ) | SRRI Score |

|---|---|

| 0 – 0.0049 | 1 |

| 0.005 – 0.0199 | 2 |

| 0.02 – 0.0499 | 3 |

| 0.05 – 0.0999 | 4 |

| 0.10 – 0.1499 | 5 |

| 0.15 – 0.2499 | 6 |

| ≥ 0.25 | 7 |

Returns Source and SRRI Calculation

- The returns used for risk metrics, including SRRI, are calculated from the official weekly NAV values published by the ETF provider:

- This approach follows EU regulatory standards, which require SRRI to be based on weekly returns derived from NAV.

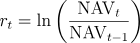

- Weekly log returns r are calculated as:

- The annualised volatility computed by:

where sigma weekly is the standard deviation of weekly log returns.

- The annualised volatility is then mapped to the SRRI risk bands to determine the final SRRI score.

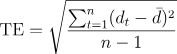

3. Tracking Error

Definition:

Tracking error measures how closely a portfolio follows its benchmark index. It is calculated as the standard deviation of the difference between portfolio and benchmark returns.

Calculation Steps:

| Step | Formula |

|---|---|

| Difference in returns |  |

| Tracking error |  |

Tracking Error Calculation

-

The tracking error is calculated over a 3-year horizon.

-

We use the annual performance data extracted from the ETF provider's official factsheet or Key Investor Document (KID).

-

The tracking error is computed as the standard deviation of the difference between the annual returns of the portfolio and its benchmark:

Updated 12 months ago