ETF Profile

ETF Risk Metrics — Formula Documentation

This document explains the mathematical logic behind the risk fields in the ETF profile API response.

1. Volatility

Definition:

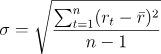

Volatility measures the dispersion of returns for a given asset. It is expressed as the annualized standard deviation of returns.

Calculation Steps:

| Step | Formula | |

|---|---|---|

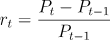

| Returns |  | |

| Standard deviation |  | |

| Annualization |  |

2. SRRI (Synthetic Risk and Reward Indicator)

Definition:

SRRI is based on the annualised volatility of returns and assigns a risk score from 1 (lowest) to 7 (highest) according to predefined bands.

Calculation Steps:

| Step | Formula (Markdown) |

|---|---|

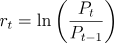

| Log returns |  |

Calculate the standard deviation of log returns and annualise as shown in the Volatility section.

SRRI Bands:

| Volatility Range (σ) | SRRI Score |

|---|---|

| 0 – 0.0049 | 1 |

| 0.005 – 0.0199 | 2 |

| 0.02 – 0.0499 | 3 |

| 0.05 – 0.0999 | 4 |

| 0.10 – 0.1499 | 5 |

| 0.15 – 0.2499 | 6 |

| ≥ 0.25 | 7 |

Returns Source and SRRI Calculation

- The returns used for risk metrics, including SRRI, are calculated from the official weekly NAV values published by the ETF provider:

- This approach follows EU regulatory standards, which require SRRI to be based on weekly returns derived from NAV.

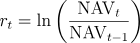

- Weekly log returns r are calculated as:

- The annualised volatility computed by:

where sigma weekly is the standard deviation of weekly log returns.

- The annualised volatility is then mapped to the SRRI risk bands to determine the final SRRI score.

For more information, please read: ESMA SRRI

3. Tracking Error

Definition:

Tracking error measures how closely a portfolio follows its benchmark index. It is calculated as the standard deviation of the difference between portfolio and benchmark returns.

Calculation Steps:

| Step | Formula |

|---|---|

| Difference in returns |  |

| Tracking error |  |

Tracking Error Calculation

-

The tracking error is calculated over a 3-year horizon.

-

We use the annual performance data extracted from the ETF provider's official factsheet or Key Investor Document (KID).

-

The tracking error is computed as the standard deviation of the difference between the annual returns of the portfolio and its benchmark:

4. ETF Dividend Yield

The ETP dividend yield represents the annual dividend income of an instrument expressed as a percentage of its current close price.

Calculation Methodology

The yield is calculated as follows:

The annual dividend is sourced from the most recent complete calendar year, defined as the latest year in which the number of dividend payments matches the instrument's most common historical payment frequency (e.g., 4 payments for a quarterly-paying ETP). If no complete year is available, the system falls back to an average of all available annual dividend figures.

The close price is mark-to-market, meaning the yield will fluctuate in line with price movements even where the dividend figure remains unchanged.

Time Frame

Calendar-year based — not a trailing 12-month (TTM) calculation.

Update Frequency

Refreshed on an end-of-day (EOD) basis. Data is updated upon each API call, ensuring both dividend figures and close price reflect the most recent EOD values.

Updated 6 months ago